At 25 years of age, musician and composer Ryan Osborne still lives with his mother in Cole Harbour, N.S., and works part-time at the Telus store at the Halifax Shopping Centre.

He’s also an investor.

In nearby Hammonds Plains, every rotation of the blades of Chebucto Wind Field’s green energy project is money in the bank for this millennial.

In 2014, Osborne took about half of his savings and invested that $5,000 in the wind energy company.

“It was something of a gamble … (but) it’s paying out really well,” he said. “Three years in, I’ve got most of my money back and it’s still going for another 12 years.”

According to the 20-something, that original investment has been giving him a return of about $2,000 per year.

Financial experts usually shy away from recommending individual stocks to young, inexperienced investors because this is often regarded as a high-risk strategy.

“If you’re an inexperienced buyer – you have a full-time job and not a lot of time to research individual stocks – then I would recommend against buying them,” said Dr. Florian Muenkel, an assistant professor at the Sobey School of Business at Saint Mary’s University.

“You should try to diversify your portfolio,” he said. “If you’re investing for your retirement in only one stock and it goes down, then there goes your retirement fund.”

Wind energy, though, is only one aspect of Osborne’s long-term investment strategy. He also has about $7,500 in CIBC mutual funds. Every month, a pre-determined amount goes straight from his bank account into that fund.

“It’s a managed fund and low volatility because I wanted that as a safety net,” he said. “It runs in the background. I let it do its thing.”

He’s also squirreling money away to buy a house. His goal? A downpayment of at least $30,000.

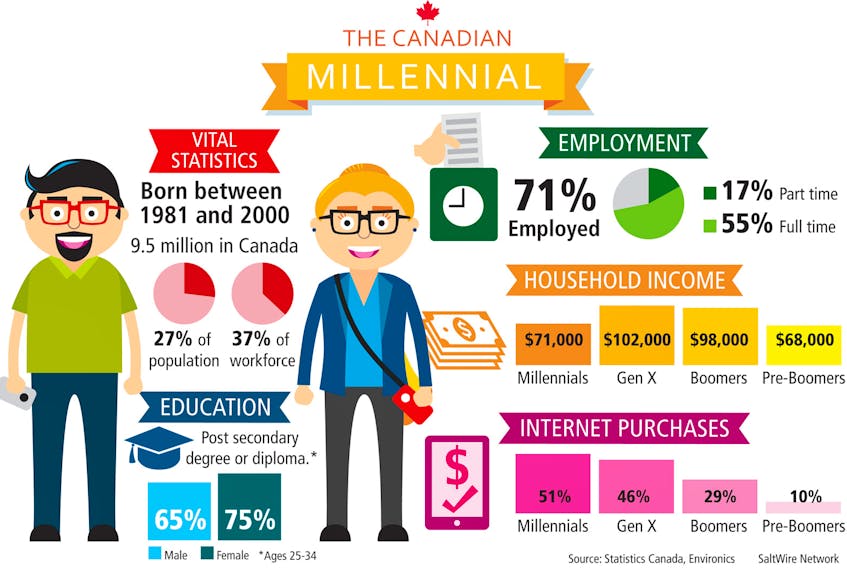

Millennials get ribbed a lot. Unflatteringly dubbed the Me generation, Time magazine described millennials on the cover of one of its issues years ago as lazy, entitled narcissists who still live with their parents – before going on to explain why they will save all of us.

In May this year, Dr. Doug Norris, a senior vice president and chief demographer at Environics Analytics, talked about millennials, calling them the next big American generation.

South of the border, there are now more millennials than baby boomers. In Canada, the millennial generation is now as big as the trend-setting boomers. And, yes, much of the negative stereotype of the millennial generation is based in fact.

Millennials are indeed much less likely to get married than their boomer parents. Members of the "me generation" – especially its young men – are also much more comfortable living at home into their 30s than were the boomers.

But millennials – especially the young women – are more educated than the preceding generations and female millennials are enjoying higher employment levels than did their mothers.

With that greater level of education, better employment prospects, and living at home, it’s perhaps not surprising that millennials are also able to save more money at an earlier age than did the boomers and to be more particular about buying brand name products. Financially, they're gaining considerable clout. And millennials are also more optimistic about the economy than any other generation.

They’re digital natives, far more at ease with technology than were their parents.

In Cole Harbour, Osborne is eyeing discount brokerage Scottrade’s online platforms, available on smartphones as well as laptop and desktop computers.

“It would take me away from the bank atmosphere and allow me to do it all on myself,” he said.

Even the stripped-down Scottrade platform for smartphones provides investment research and market news, watch lists, real-time streaming of quotes, and trading of stocks, options and exchange-traded funds, usually called ETFs.

These are marketable securities that trade like common stock on the exchanges and track an index, a commodity, bonds or a basket of assets.

According to Muenkel, the typical performance to investors of these passive ETFs is actually higher than that of that of professionally managed mutual funds once all the fees are factored in.

“The (managed mutual) funds that do well in one year generally don’t outperform the market in subsequent years,” said Muenkel. “(The performance of ETFs) compared to these actively managed funds is actually better.”

Scottrade generally charges $6.95 for each trade of stocks or ETFs through its online platforms, adding another fee for the highly speculative penny stocks.

But the future of online trading may soon explode with the arrival of even lower-cost tools. South of the border, a trading app called Robinhood is targeting millennials with completely free online trading.

Here’s how Robinhood works. Once the user has filled out an application and been accepted, the company zips off an introductory video explaining what the app’s sleek interface can do: buy or sell at market price, place stop loss and stop orders, or make limit orders.

There’s no minimum account requirement.

That ease of use and zero cost for trading is leading to changes in the way millennials in the United States are trading through Robinhood.

Vlad Tenev, the company’s founder, has reportedly claimed Robinhood is leading millennials to buy just of few shares at a time of dozens of different stocks and then hang onto them, essentially building up their own diversified portfolios without any direct advice from brokers at all.

Those apparently don’t feel they need a broker’s advice.

“Millennials have more access to information than at any other point in history,” said Muenkel. “It’s never been as easy to find information … (and) they’re comfortable getting information on their own.”

The finance professor cautions, though, any information anyone finds, either on the net or elsewhere, should always be checked for accuracy.

Industry insiders are still waiting to see what the impact of low-cost, online trading platforms will be on investors, particularly inexperienced ones.

“There are reasons why financial advisors are around,” said Muenkel. “Even if they don’t provide information on assets … they can serve the function of reigning you in when you’re sitting there wondering if you should sell.”

Studies show individual investors tend to sell even well-performing stocks too early and hold onto poorly performing stocks too long. It’s called the disposition effect and it comes from a tendency to think we’re right and others are wrong. In the world of stock trading, that can lead to significant financial losses.

Despite the inherent dangers in trading in individual stocks for inexperienced investors, it’s clear that the trend to lower-fee, discount brokerages and no-fee, online trading platforms is only going to heat up.

As with most things, the key to success is mastering the basics at an early age.

Osborne, whose mother is an accountant with the provincial government, got the basics of financial literacy taught to him at an early age. When he was only seven, his mother opened up a bank account for him. Then, she taught him how to budget.

“I started budgeting when I was 14 or 15 years old because I knew I wanted to go to college for music. So, I put my money in guaranteed investment certificates … I tried to save 25 per cent of everything I made,” said Osborne.

Since then, the financially literate millennial has tried to pass on that knack for money management to his friends – many of whom are astonished he can afford to go on trips to exotic locales – and taught them how to budget to save up for the things they want.

It’s not for everyone.

“I love Excel spreadsheets. I live off of those,” said Osborne. “But other people look at that and can’t change their behaviour. It stresses them out.”

His advice?

“Start small,” he said. “Little amounts here and there, especially when you’re young and don’t have a family.”